Money matters

Special Fixed Deposit Schemes For Seniors

Samyuktha Vibhu, a Certified Financial Planner (CFP) at ithought Advisory guides you through the best fixed deposit schemes available for you to invest. Read it and make an informed choice.

Karan and Neha usually weren’t the kind to worry about money. For more than a decade they had led a comfortable retired life. But, in the last four years, FD returns had plunged while inflation remained steady. In their early retirement years, well-reputed companies widely offered 8-9 per cent on their FDs. However, recently, Neha saw only small Finance Banks, Non-Banking Financial Companies (NBFC) and lesser-known corporates offering these levels of returns. She sought comfort in reliable names and government-linked schemes. Karan on the other hand was contemplating moving out of fixed deposits and into bonds. So, what were their best investment options?

Best fixed deposit schemes available for seniors now

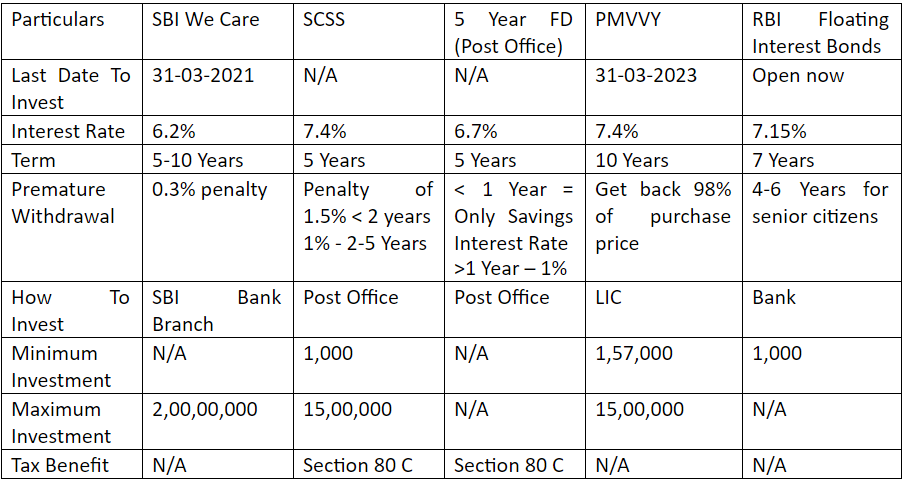

Karan and Neha identified 5 safe investment options for resident seniors across bonds, fixed deposits, and pension plans. Here’s a quick snapshot of what they found:

Let’s take a closer look at each of these options.

SBI We Care or SBI Special FD For Senior Citizens

This is a scheme launched by SBI for resident senior citizens only. On regular Fixed Deposits, seniors are eligible for an additional interest rate of 0.5 per cent. With the SBI We Care deposits, seniors get an additional 0.3 per cent interest. The deposits under this scheme range from 5-10 years. A senior can start a fresh deposit or renew an old one. The window of opportunity for this scheme is open until March 31st 2021. Seniors can open We Care deposits through the SBI Yono App or at the bank. If the deposit is withdrawn before it matures, then they lose the additional interest of 0.3 per cent.

Karan and Neha liked this option because they received a 6.2 per cent return from a Public Sector Bank like SBI on a 5-year FD. More importantly, unlike the other savings schemes, the cap on investments was at 2 Crores and not a few lakhs. They had to reach out to SBI to understand their interest payment options (i.e. half-yearly/yearly).

Senior Citizens Savings Scheme (SCSS)

The Senior Citizens Saving Scheme is a popular choice amongst retirees. Investors can start with a minimum of Rs. 1,000 and go up to a maximum of Rs. 15 lakhs. Interest from these deposits is paid out every quarter. The SCSS is offering an attractive interest rate of 7.4 per cent. After the initial period of five years, the account can be extended for another 3 years. Neha was an advocate for the SCSS because it was a post office scheme with tax benefits under Section 80 C. In a market where they were hunting for returns, the SCSS offered the best of both worlds. She went in with her eyes open knowing that she’d lose 1-1.5 per cent of her interest if she withdrew the deposit before it matured.

5 Year Post Office Time Deposit

As the name suggests, this is also a post office scheme and it’s a five-year FD. With post-office time deposits (fixed deposits) there is a lock-in of six months. After six months, the investment can be prematurely withdrawn by paying a penalty of 1 per cent. The interest on the 5 Year FD is at 6.7 per cent. Interestingly, the five-year FD is eligible for deduction under Section 80 C.

Pradhan Vaya Vandhana Yojana (PMVVY)

The PMVVY scheme was launched as a pension scheme for senior citizens. You can purchase it through LIC. The investor can choose to receive a monthly, quarterly, half-yearly, or annual pension. The minimum monthly pension is Rs. 1,000 and the maximum is Rs. 9,500. Senior citizens can invest between Rs. 1.5 Lakhs to Rs. 15 Lakhs in the scheme. Upon maturity, the initial investment is returned to the investor. The scheme is open for investments until March 31st, 2023. Karan liked this scheme because it ensured regular income at a reasonable rate for the next ten years. The policy allowed exit only under certain extreme circumstances, so he was mentally prepared to stay invested for a decade. Karan understood that he’d get 98 per cent of his purchase price (initial investment) back if he exited the policy early.

RBI Floating Interest Bonds

An interesting investment Karan and Neha came across was the RBI Floating Interest Bond. These 7-year bonds were issued by the RBI on behalf of the government. The interest offered on these bonds was 0.35 per cent more than that of the National Savings Certificate. This interest would be reset every six months. So, this meant that there was no “guaranteed” or fixed return. Floating rate instruments deliver more returns in an upward cycle and less in a downward cycle. As senior citizens, they had the option of withdrawing investments before they matured. They wouldn’t be able to sell or trade these bonds. There was no maximum investment limit, and they could easily buy these bonds at their bank. Karan and Neha were ready to try a new safe investment in bonds that were guaranteed by the RBI.

Karan and Neha found a few safe and interesting investment options. Although they hadn’t reached their 8 per cent dream, things were looking up for them. Consult a financial planner or investment adviser before making any investment decisions.

Comments

Anonoymous

11 Jul, 2014

[…] Click here to read: Special Fixed Deposit Schemes For Seniors […]

Hemalatha

18 Jun, 2014

Really very useful tips..TQ.

Post a comment